A Whole Life vs. Universal Life Insurance policy can help your loved ones with their struggles with money issues when you die. However, with so many insurance options, it looks pretty challenging to select the correct type of policy for you.

The more one knows about life insurance options, the better equipped one is to choose the best life insurance.

One of the challenges you might face when buying life insurance is the Whole life vs. Universal life insurance. What do you think these two types of life insurance are, and how can one discover which policy is the best?

See the following subheading and find out the differences between the Whole Life and Universal Life insurance.

The Basic Differences Between Whole Life and Universal Life Insurance

To note, permanent life insurance has two types of life insurance, which include Whole Life insurance and Universal Life insurance.

Permanent life insurance keeps on functioning as long as you pay premiums, and cash value increases over time. While you’re alive, you can tap into a policy’s value.

Even though the two types of life insurance are permanent life insurance, they both vary in many ways, and this includes costs, premium flexibility, cash value growth, and the death benefit.

Major Differences Between Whole Life and Universal Life Insurance

Let’s find out more about Whole Life insurance…

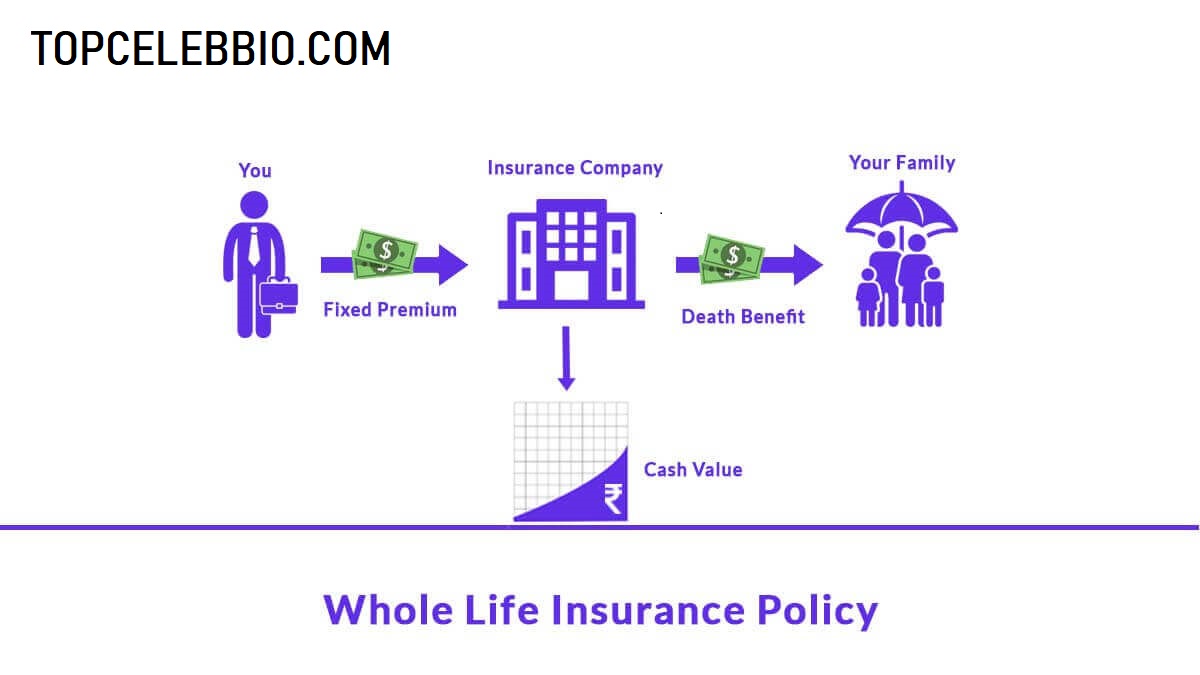

Whole Life Insurance

Whole Life Insurance seems to be a permanent life insurance policy that has fixed premiums and death benefits. The cash value within a whole life insurance policy increases at a fixed interest rate, which is 2%, and this gives whole life more predictability than universal life policies.

Pros & Cons of Whole Life Insurance

Pros

- Fixed premium, death benefit, and rate for cash value growth.

- Offers low risk.

- Easiest type of permanent life insurance to navigate because everything is fixed and easy to understand.

Cons

- Doesn’t provide flexibility to change premiums or the death benefit amount as your needs change.

- Premiums can be very expensive compared to other types of life insurance.

- Can build less cash value than some types of universal life insurance.

Benefactors of the Whole Life Insurance

If you want guarantees and a cash value that increases consistently, whole life insurance can be a wise choice.

If your primary need for life insurance is to cover long-term costs like your funeral, your whole life can be an appropriate choice. For instance, whole life insurance plans are often low and used for burial insurance.

The predictability of whole life insurance may also be helpful to someone who doesn’t want to be obligated to make investing decisions but wants to make use of a future life insurance payment for the care of a lifetime financial reliance, such as a kid with special needs.

A Special Needs Trust (SNT), which is a legally binding arrangement often made by a parent or guardian, could contain this whole life insurance. The funds are kept in an account and are used for the child’s maintenance.

Universal Life Insurance

This type of permanent life insurance enables you to adjust both the premiums and the death, unlike whole life insurance which is fixed. However, universal life insurance has certain limits to its adjustments, it can also grow cash value.

In universal life insurance, the rate of growth determines the type of universal life insurance you get:

- Guaranteed universal life insurance: If there is a cash value component, growth may be minimal, but this type of policy provides a lower-cost way to secure lifelong coverage.

- Indexed universal life insurance: Cash value growth is tied to a specific index, such as the S&P 500.

- Variable universal life insurance: You choose investment sub-accounts, and your cash value gains depend on investment performance.

Pros & Cons of Universal Life Insurance

Pros

- More flexibility by allowing you to adjust premiums and the death benefit.

- A variety of types of universal life insurance lets you choose a policy that best fits your life insurance preferences.

- An indexed or variable universal life insurance policy may gain more in cash value than whole life.

Cons

- Selecting sub-accounts in a variable universal life insurance policy needs knowledge about those investments and active policy management.

- An indexed universal life insurance policy’s participation rates and caps can limit your cash value growth potential even when the markets do well.

- A variable universal life insurance policy’s success is linked to sub-account decisions, which may not interest people who don’t want to be actively engaged in investment decisions.

Who Can Benefit From Universal Life Insurance?

If you want a flexible permanent life insurance coverage that allows you to adjust the death benefit and premium based on your current financial condition, universal life insurance can be an excellent decision.

It can also be the right choice for someone who wants to play a more active part in selecting their assets.

Which Costs More: Whole Life or Universal Life Insurance

Obviously, Whole life insurance costs more than universal life insurance. As a unique rule, you’ll pay about twice as much for a whole life vs. universal life insurance.

Below’s an example of our analysis of monthly whole life & universal life insurance premiums for both men & women in good health who don’t make use of tobacco.

The average is best on the three lowest quotes that was found online for nonsmokers of average height and weight.

Whole Life vs. Universal Life Insurance: Which Is Right For You?

Be it Whole life or Universal life, it’s better if it comes down to your desired stability or flexibility.

Those who value stability and guarantees might be more attached to a whole life insurance policy. Precisely, you should know how of a death benefit your loved ones will receive, and your premiums will not change as long as you have a policy to keep up with.

Furthermore, a whole life insurance policy constantly accrues cash value that you can use when necessary.

Similarly, revenues from mutual life insurance companies are often paid to policyholders and can be used to either increase cash value or lower rates. You need to pay for all of these benefits.

Sarrubbo Says:

Whole life is ideal for individuals who want guarantees and the ability to accumulate savings.

On the contrary, a universal life insurance policy can be a better option if you value flexibility. As your life circumstances change, you may want to be able to adjust your life insurance policy.

For instance, with a universal life policy, you can increase your premium payments during good times or lower them in the event of a job loss or other financial difficulty.

To create a personal financial strategy, it is essential to meet with a financial counselor.

Then, you’ll be able to see which kind of life insurance best suits your goals. It could turn out that all you want is a basic term life insurance policy.

Source: TopCelebBio